Discipline is Hard

I left home on Wednesday, and I won’t be back for more than a month. When my son’s daycare offered us the option of enrolling for the month of July, we saw an opportunity to get away from the brutal heat and humidity of summer in New Orleans. We will be visiting friends and family throughout Alabama, western North Carolina, and North Georgia – cooler parts of the southeast – for a few weeks. The whole family is on this trip, including our four-year-old pitbull. At the end of July, I am visiting Joey Fishman in our Portland, Oregon office for a week. I can’t wait for that trip, but more on that in another post.

I am lucky that I can work from anywhere with an internet connection, so I don’t have to take a month of vacation to take this journey. My hope is that writing will be easier on the road, away from the chores and distractions of everyday life. I am very excited to meet a few clients in person for the first time during my travels.

One of my greatest challenges during this month will be keeping up with my yoga practice. Since I won’t be attending classes at a studio, I have to adopt a home practice. Home practice is actually a big part of the yoga method I follow, which is called Ashtanga yoga. The first westerners to study Ashtanga travelled to India for months at a time to practice with their teacher, Pattabhi Jois. After learning a new series of poses, they returned home, often for more than year to practice alone at home, until they saved enough to return to India. Back then, there were very few yoga studios in the U.S, let alone teachers in the Ashtanga method.

Although I’ve been practicing Ashtanga for almost 10 years, I never developed a successful home practice. Without a teacher watching over me, and fellow students practicing beside me, my mind wanders. I often skip my least favorite poses and find myself quitting early. This month will be a test of my discipline. As I roll my mat out in tight spaces and between furniture in different houses, it is going to take sheer willpower to finish my practice most days. But, I am determined to do it. I don’t want to return to New Orleans next month stiff as a board and out of shape.

Discipline is Hard

In investing, discipline is especially difficult. The last decade is a perfect example. Since the bottom of the 2008-2009 Financial Crisis, anything an investor did to diversify risk away from S&P 500 Index detracted from performance. Long-time staples, backed up by oodles of academic research, like the size and value premium, haven’t worked. This has been going on for a decade. A child born in 2009 will be entering 4th grade in the fall. Ten years is a major test to a diversified investor’s discipline.

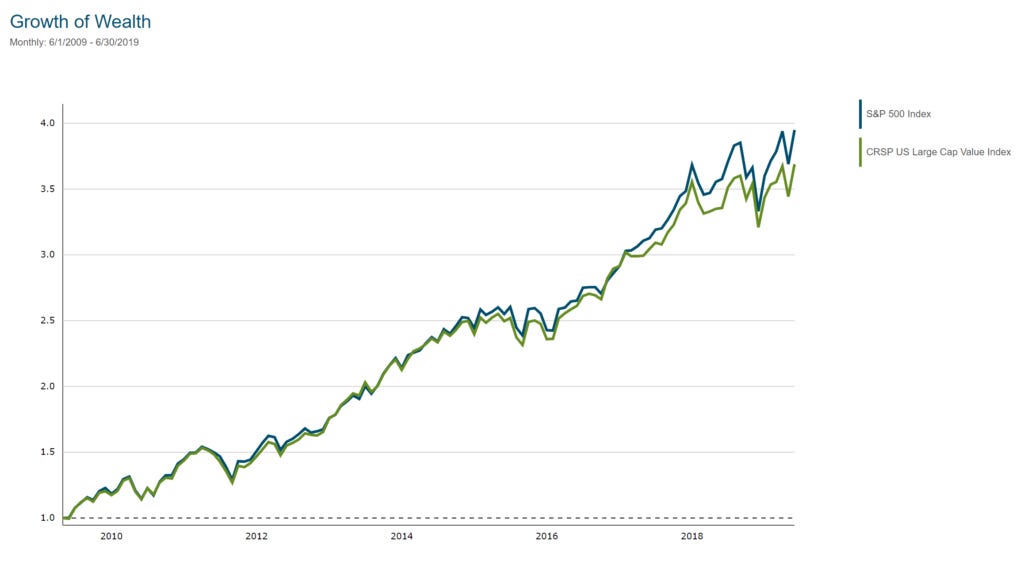

Below is the 10-year chart of the S&P 500 Index versus the CRSP (The Center for Research in Security Prices) Large Cap Value Index. If I add a growth index to the chart, the under performance looks much worse. When Fama and French wrote their 1993 paper on the 3-factor model, they illustrated that low-priced stocks (value) outperform high-priced stocks (growth) over virtually all long-term market cycles. They found the average outperformance of value stock to be an astounding 0.40% per month! Intuitively, it makes sense that an investor should expect a higher return for buying a lower priced security than for buying a higher price one. Buy low, sell high – right?

Ten years is a long time to explain to clients that value should eventually outperform. Has something fundamentally changed in markets that we missed? Josh made a very solid argument that it might have here. But value investors have felt this kind of pain before, in the late 90’s. When internet stocks were trading at 600 times non-existent earnings, everyone thought Warren Buffett was a sucker. We all know they were wrong and that tech stock valuations returned to Earth during the Dot.com crash. History doesn’t repeat, but it sometimes rhymes.

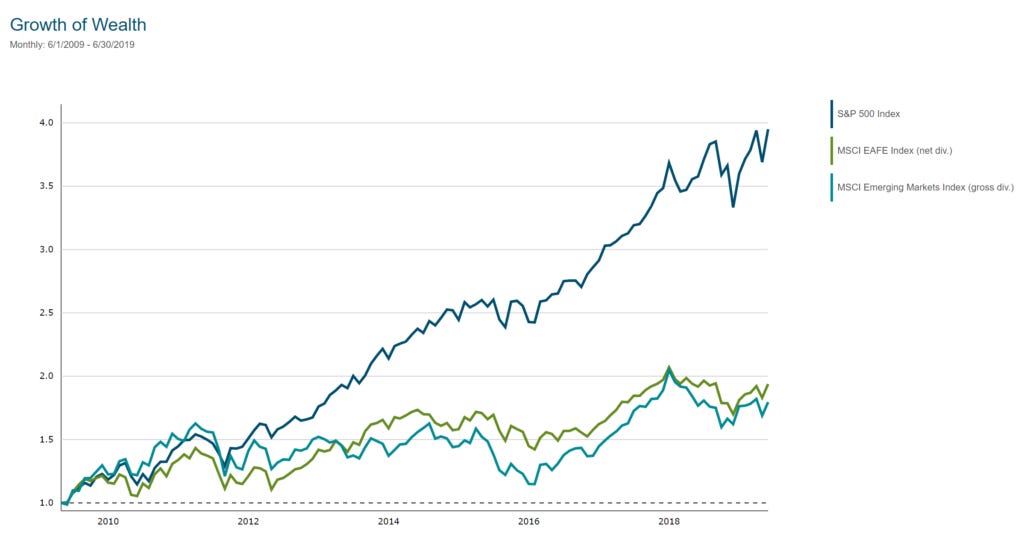

The pain is worse for investors who are diversified internationally. Below is the 10-year chart of the S&P 500 Index versus the MSCI EAFE (International Developed Stocks) and the MSCI Emerging Markets Index. Ouch! A dollar invested in the U.S. is worth more than twice as much as a dollar invested internationally. The U.S. stock market comprises about 51% of the total world stock market. Eliminating the other 49% would entail taking a massive bet, albeit one that has paid off in spades for the past decade, and is not something that a professional, prudent investor would do. It is highly unlikely the U.S. stock market can continue this type of outperformance forever.

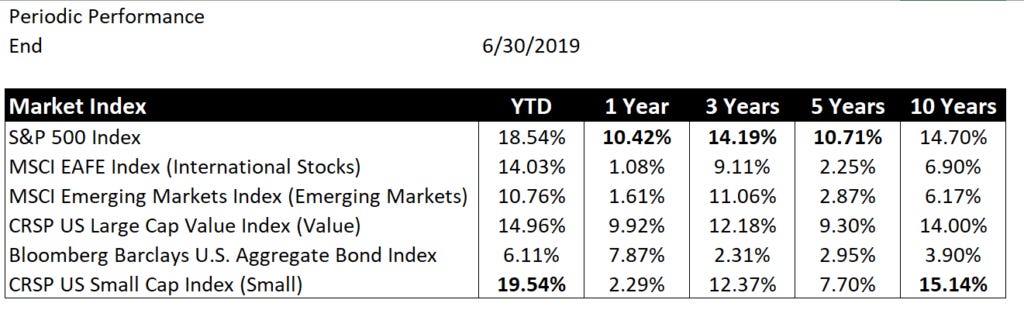

Practically anything an investor has done to diversify their portfolio over the last 10 years has hurt performance. In a strong bull market, we expect bond performance to lag. The only ‘premium’ that has worked is the small cap premium, but small caps just barely outperformed large cap stocks over the last decade. Take a look at the next chart. Over the past year, International and Emerging Market stocks have lagged the S&P 500 Index by 9%, and small caps lagged large caps by more than 8%. These are very wild disparities among stock index returns.

There’s an old adage that “Diversification means always having to say you’re sorry” for something in the portfolio that is dragging down performance. But 10-year periods of underperformance test the wills of even the most disciplined investors. Discipline is difficult by design. Only those with the mental and physical strength to persevere will reap the rewards of their dedication. If it were easy, everyone could do it.

The post Discipline is Hard appeared first on The Belle Curve.