Paying for Healthcare

It’s no secret that healthcare costs are rising faster than wages. Employers have shifted more of the burden of health care premiums to employees. Deductibles are higher, and coinsurance rates are lower. We are paying more for less coverage. This trend is not likely to reverse anytime soon. There is a tax-advantaged method of savings for health costs called the Health Savings Account or HSA. In my opinion, HSAs are vastly under utilized and do not receive enough credit for their benefits.

A 2016 study found that only 20.2 million Americans have a Health Savings Account. HSAs were created by the Medicare Modernization Act of 2003 and first became available in 2004. Participants save pre-tax dollars, grow tax deferred, and withdrawals for qualified healthcare expenses are tax-free. This triple tax-advantaged status makes HSAs a compelling option.

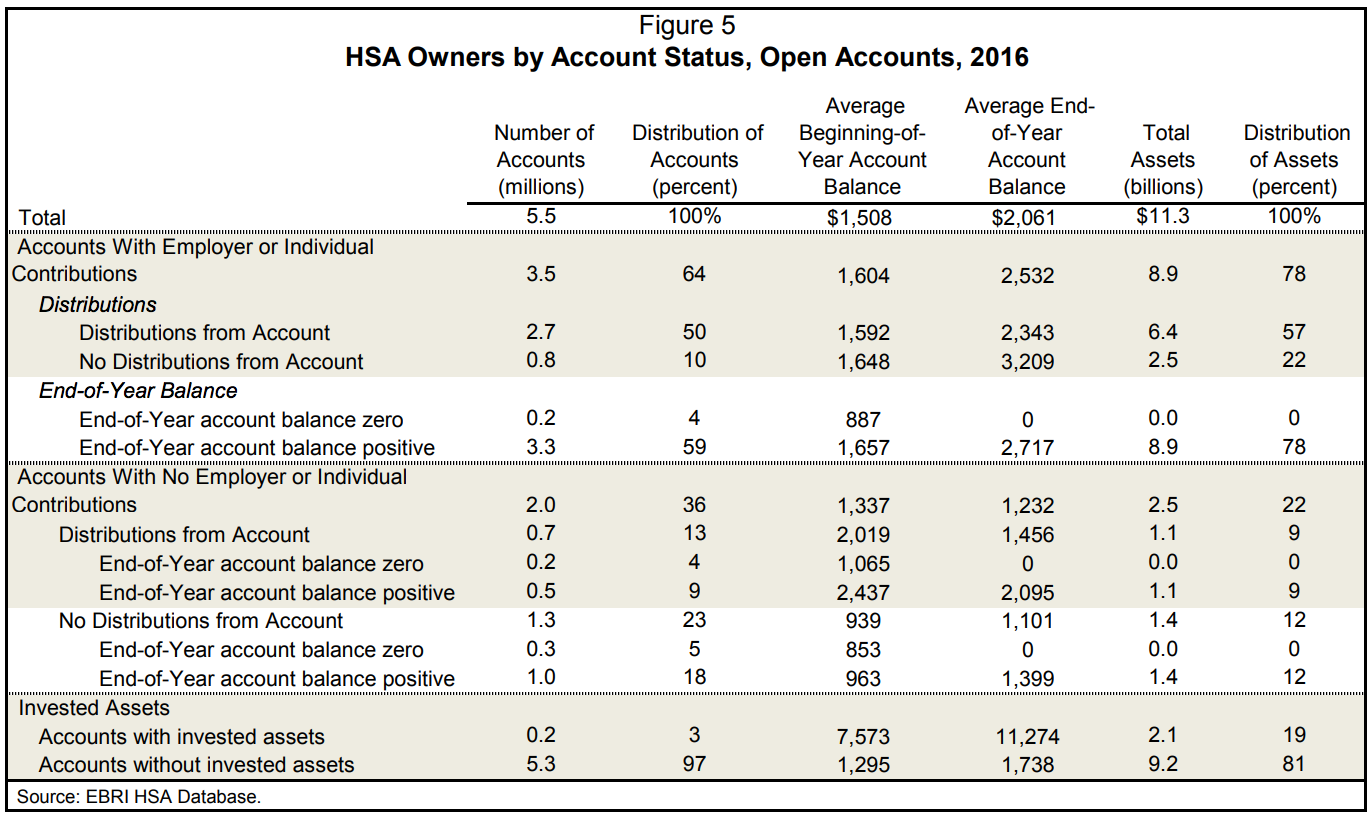

Unlike its predecessor, the Flexible Spending Arrangement (FSA), which must be spent each year, HSA accounts can accumulate over time. Funds within an HSA can be invested in stocks and bonds, creating and IRA type account for future healthcare costs. However, the Employee Benefit Research Institute (EBRI) found that less than 4% of HSA participants invest their funds in something other than cash.

Below is a chart from the EBRI study. At the bottom, you can see that the average HSA account balance for those with investments was $11,274 versus $1,738 for accounts invested solely in cash.

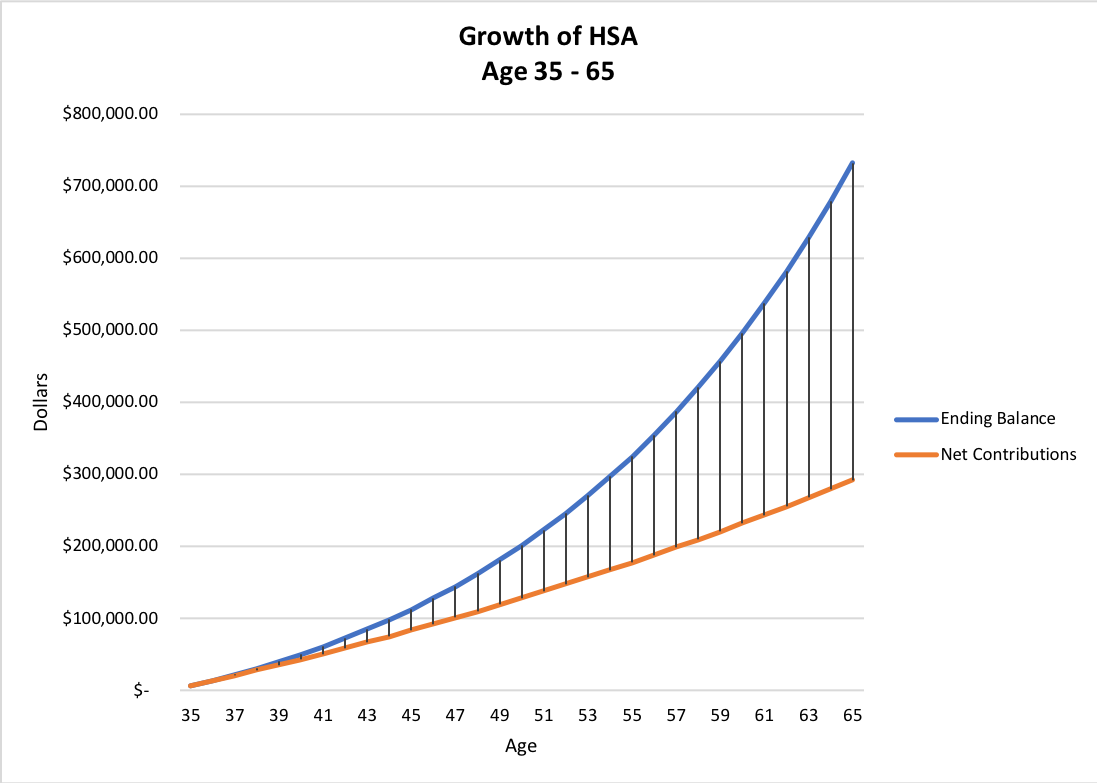

In 2018, the max contribution to an HSA for a family is $6,900, with a $1,000 catch-up for individuals 55 and older. Assuming a 2% annual increase in contribution limits, and a 6% average rate of return on investments, a 35-year-old who maxes an HSA account every year until age 65, could accumulate more than $700,000 in the account. Total contributions over thirty years were $292,000, with and an estimated cumulative tax savings of $96,000.[1] Medicare premiums, out-of-pockets expenses, and long-term care insurance premiums are all considered qualified expenses. Funds can be withdrawn tax-free to pay for these in retirement.

Why are so few people using Health Savings Accounts? First, they require the participant to enroll in a high deductible heath policy (HDHP) to contribute. In 2018, the minimum deductibles are $1,350 for singles and $2,700 for families. Even though the health insurance premiums are lower, many participants do not want to be responsible for high out-of-pocket health care expenses. The health insurance market has shielded us from the underlying costs of medical procedures, and for some, this change is too dramatic. People with chronic illness or multiple young children may be better off in the short-run by choosing a plan with a low deductible. I would argue that high income earners should max an HSA and pay for medical expenses with after-tax dollars, allowing the HSA balance to grow.

Medical costs are one of the biggest expenses in retirement. If retiring before Medicare, the cost of buying private health insurance is astronomical. A couple aged 60, can easily expect to pay $25,000 – $30,000 a year for health insurance. Even those who work until Medicare eligibility at age 65 can expect to pay $6,000 – $8,000 per individual per year to cover Medicare premiums, Medigap coverage, and out-of-pocket expenses. Wouldn’t it be nice to save for these expenses in advance, through triple tax-advantaged Health Savings Accounts? Even though withdrawals for healthcare costs along the way diminish the accumulation potential, at least these expenses get paid with pre-tax dollars.

Critics of HSAs point out that they overwhelmingly benefit the wealthy who can afford to defer income each year. The critique is accurate but not a reason to eliminate HSAs. Health Savings Accounts will not solve the societal problem of paying for healthcare for those who cannot afford it. But they are a fantastic way to save pre-tax for current and future healthcare expenses.

[1] Assumes a federal tax rate of 28% and state tax rate of 5%.

The post Paying for Healthcare appeared first on The Belle Curve.