The Superpower of Saying No

Modern life feels like a constant pursuit of more. In childhood, we seek more education, building a foundation of knowledge and skills to enter adulthood. We begin a career and climb a never-ending ladder of promotions, titles, and raises. With those raises, we accumulate more things: houses, cars, furniture, clothes, and gadgets. If we start a family, the stuff we purchase compounds as children progress through new sizes, interests, and activities. The hedonic treadmill is a race that will not end until the mouse stops running.

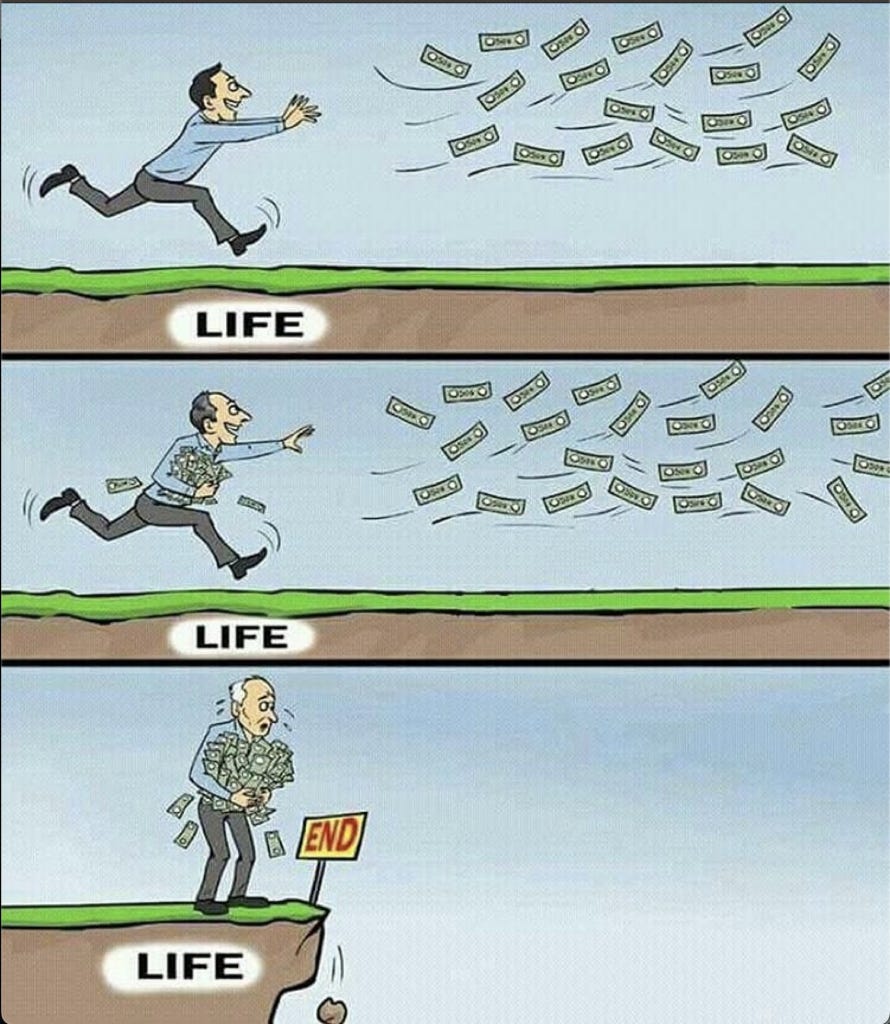

Likewise, we are taught to save money and invest for the future. Our retirement nest eggs must accumulate and grow to never-ending proportions. We can never have enough, and our portfolio returns must be higher than the overall market. We must be the best, or at least better than our neighbors. This script is so embedded in our psyche that most retirees never spend their savings and have more money at the end of life. There’s always more to pursue around the next corner. More, more, more.

Lately, I’ve been interested in less. This does not come naturally to me. Like many modern-day humans, I have been programmed to constantly strive for the next achievement, goal, or pursuit. I believe this societal pressure compounds for American women who are brainwashed to believe we must ‘have it all’—the career, the family, the clean house, the perfect wardrobe, hair, and makeup. We should have our cake and cook it, too.

Saying no is a superpower, however. I am impressed by anyone who finds it easy.

A few months ago, I realized I was oversubscribed with volunteer activities. Let’s be honest my career and my family are both full-time careers unto themselves. Throw in a few nonprofit boards, fundraisers, and committees, and I no longer had time for what matters most.

With this mindset, I joined the Ritholtz Wealth book club, organized by our Chief of Staff, Anna Chaiken, to read: Four Thousand Weeks: Time Management for Mortals. Rather than preaching traditional time management techniques, the book suggests to simply stop trying to do it all. I turned our book club discussion into a personal therapy session by admitting I was oversubscribed with activities. Finally, Tony Isola charged me with resigning from at least one board within the next week. And guess what—I did it.

After the anxiety wore off, I felt an enormous sense of relief. Since then, I have felt fewer qualms about turning down additional opportunities. I am still a work in progress, but I am resolute to continue saying no and letting go of anything that is no longer absolutely essential.

This concept applies to building and managing financial plans. Fewer goals can allow for faster financial independence. A simpler investing plan carries less administrative burden and lower cost. Time, after all, is our most precious resource, and none of it is guaranteed. If we live to age 80, we have 4,000 weeks. How do we want to spend them? How many have already passed?

Rather than thinking about what to add to my plate, I want to focus on what to take away. It’s a contrarian mindset that challenges modern societal norms, but perhaps it is the gateway to a more meaningful existence.

The post The Superpower of Saying No appeared first on The Belle Curve.